Global Smartphone Race: Samsung, Apple and the Rise of Chinese Rivals

SammyGuru is reader-supported. We have affiliate and sponsored partnerships, so we may earn a commission when you buy through links on our site — at no extra cost to you. Learn more.

For over a decade, Samsung and Apple have remained the twin pillars of the global smartphone industry. Their rivalry has defined the modern smartphone era, with both companies trading leadership positions quarter after quarter. Yet, the balance of power between the two has been anything but static, shaped by shifting product cycles, evolving consumer demand, and the rapid rise of Chinese competitors.

Quarterly swings and launch cycles

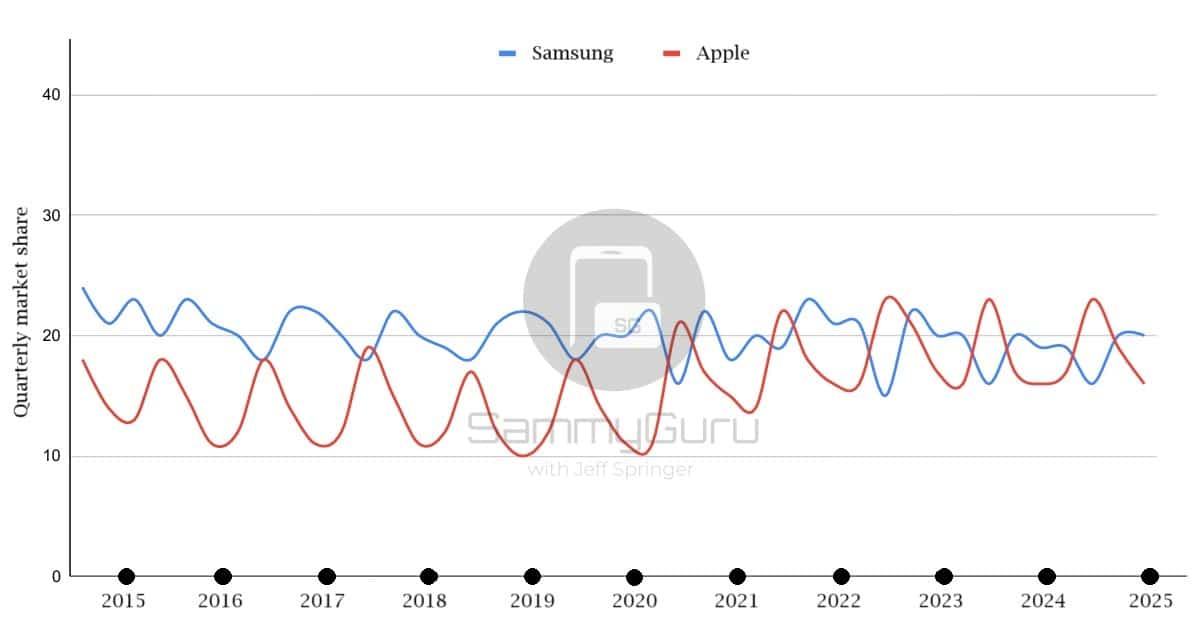

The global smartphone market is highly cyclical, and nowhere is this more evident than in the competition between Samsung and Apple. Each year, Apple’s market share soars during the fourth quarter, coinciding with the launch of new iPhone models ahead of the holiday season.

In Q4 2024, Apple captured 23% of global smartphone shipments, overtaking Samsung’s 16%. This pattern has remained consistent — Apple benefits from massive year-end demand in North America and Europe, where high consumer spending and brand loyalty drive strong iPhone sales.

By contrast, Samsung typically regains the lead in the first quarter, fueled by the launch of its latest Galaxy S series and a wide lineup spanning from premium flagships to affordable Galaxy A and M series phones. In Q1 2025, Samsung reclaimed the top position with a 20% share, while Apple slipped to 19%.

This alternating dominance underscores the different strategies each company employs. Apple has historically relied on a concentrated lineup of premium devices and a tightly integrated ecosystem. Samsung, meanwhile, maintains a diverse portfolio across multiple price tiers, allowing it to tap into both mature and emerging markets.

Samsung is struggling to hold ground in a crowded Android space

While Samsung continues to lead in annual smartphone shipments, its overall market share has gradually declined over the past decade. The South Korean giant’s broad Android lineup remains popular, but intense competition from Chinese brands has eroded its dominance in the mid-range and entry-level categories.

Manufacturers such as Xiaomi, Oppo, Vivo, and Transsion (the parent company of Tecno and Infinix) have rapidly gained ground, especially in Asia, Africa, and Latin America. Their strategy of combining aggressive pricing, modern designs, and feature-rich hardware has enabled them to capture consumers who seek value-driven alternatives to Samsung’s mid-tier offerings.

Moreover, Transsion has emerged as a dominant force in Africa, while Xiaomi and Vivo lead in markets like India. Samsung’s challenge now lies in defending its share in these price-sensitive regions without diluting the appeal of its flagship models.

Despite these pressures, Samsung’s innovation pipeline remains strong. The company continues to push the boundaries of mobile hardware with foldable phones, advanced camera technology, and custom Exynos chipsets. Its dominance in components such as displays and memory chips also provides strategic leverage over competitors.

Apple’s steady rise and ecosystem advantage

Apple, meanwhile, has maintained a steady upward trajectory in market share over the long term. Its focus on the premium segment has insulated it from price wars. Moreover, its ecosystem spanning iPhones, Macs, iPads, Watches, and services ensures customer retention at unmatched levels.

In recent years, Apple has also made deeper inroads into emerging markets like India and Southeast Asia, previously dominated by Android brands. With strategies such as localized manufacturing and retail expansion, Apple is positioning itself to tap into the next wave of smartphone growth.

Huawei’s rise and fall

No discussion of the smartphone market would be complete without mentioning Huawei, once poised to overtake both Samsung and Apple. Before U.S. sanctions in 2019, Huawei briefly overtook Apple to the second position, thanks to its strong momentum in China and Europe. However, restrictions on accessing U.S. technologies, including Google Mobile Services and advanced chips, severely crippled its international business.

Today, Huawei has rebounded domestically with its self-developed HarmonyOS and Kirin chipsets, but its global footprint remains limited. The vacuum it left behind has largely benefited other Chinese players, and to some extent, Apple, in the high-end segment.

As 2025 unfolds, the battle between Samsung and Apple is expected to continue its familiar rhythm, with Apple dominating late-year sales and Samsung rebounding early in next year. However, both companies face mounting challenges from increasingly capable rivals, market saturation in mature regions, and a slowdown in global smartphone replacement cycles.

Written by

Sumit AdhikariSumit, a life-long Samsung user, is passionate about technology and has been professionally writing on tech since 2017. He’s a mathematics graduate by education and enjoys teaching basic mathematics tricks to school kids in his spare time. Sumit believes in artificial intelligence and dreams of a fully open, intelligent and connected world.

Follow us on Google Discover & set us as a preferred source in Google News

Share this Post

___________________________

New Blog Posts

___________________________

First Set of Pixel 11 Pro XL Renders Are Here

Pixel 11 Pro XL CAD renders show minimal design changes

Is Samsung Preparing One UI 8.5 Beta for Galaxy Z Fold 5 and Flip 5?

Samsung may launch a One UI 8.5 beta program for its 2023 foldables

Galaxy S25 One UI 8.5 Beta May Run Longer Than Expected

Galaxy S25 series’ One UI 8.5 beta may stretch to 10 rounds